Russia Oil Production

Russia Oil Production

Is Russia's invasion of Ukraine primarily about capturing Ukraine's resources to finance Russia's military? Is the Ruso-Ukrainian war strictly about resource ownership?

Russia’s invasion of Ukraine provided me encouragement to start posting my analytics to this website.

I am reluctantly in retirement. I loved my job as Vice-President of Gas Strategy and then Chief Gas Strategist at Sempra LNG for the past 20 years. Thus far I have limited my post-retirement distribution to former Sempra colleagues, the US Potential Gas Committee (where I am an observer) and the EIA. But as the democratic world (beyond Ukraine) might soon be at war with Russia, it might be useful to broaden the audience.

This first edition focuses exclusively on Russian Oil. There seems to be a great amount of confusion about the reasons why Russia is invading Ukraine. I thought it might be worth adding one more voice to the chorus. Hubbert Math analytics suggest that Russian crude oil and condensate (C&C) production rate is peaking. EIA’s International Energy Outlook 2021 forecast also suggests that Russia’s oil production rate has peaked. My outlook differs from that of EIA in that I do not believe Russia can reverse its decline. The rate of Russia’s oil production rate decline is still uncertain, but there is reason to believe that the decline could be more severe than what I am forecasting. Analysts tend to error on the side of conservativism.

My analysis of global oil and gas is based on Hubbert Math. Hubbert Math has been debated thoroughly in the press and I will not review the pros and cons of M. King Hubbert’s methodology here. If you are interested, Jon Claerbout and Francis Muir, two retired Stanford Geophysics Department professors, published an excellent update paper in 2020, which is available on the internet. Claerbout and Muir’s paper provides the mathematical basis for this work.

I have conducted Hubbert Math analytics for every play, field, state/province and country that I can develop a high confidence history of cumulative production. I have compared Hubbert projections against ultimate recovery estimates implied by EIA, BP & other government reserve estimates. I have done this analysis for crude oil and condensate (C&C), natural gas liquids (NGL) and natural gas. The plots below presume some understanding as to how oil industry professionals think about resource exploitation. If there is sufficient interest in this work, I will provide more commentary.

The plots below are current through November 2021. The data sources are EIA’s monthly postings and the US Bureau of Mines Yearbooks from 1930 to 1976. Breakdown of former Soviet Union (FSU) production prior to 1991 is made by first subtracting out Azerbaijan’s annual production history, which goes back to its beginning of production (1871). Selected years are reported in literature for some FSU states. Production profiles for those states are constructed based on limited data. The residual is assigned to Russia.

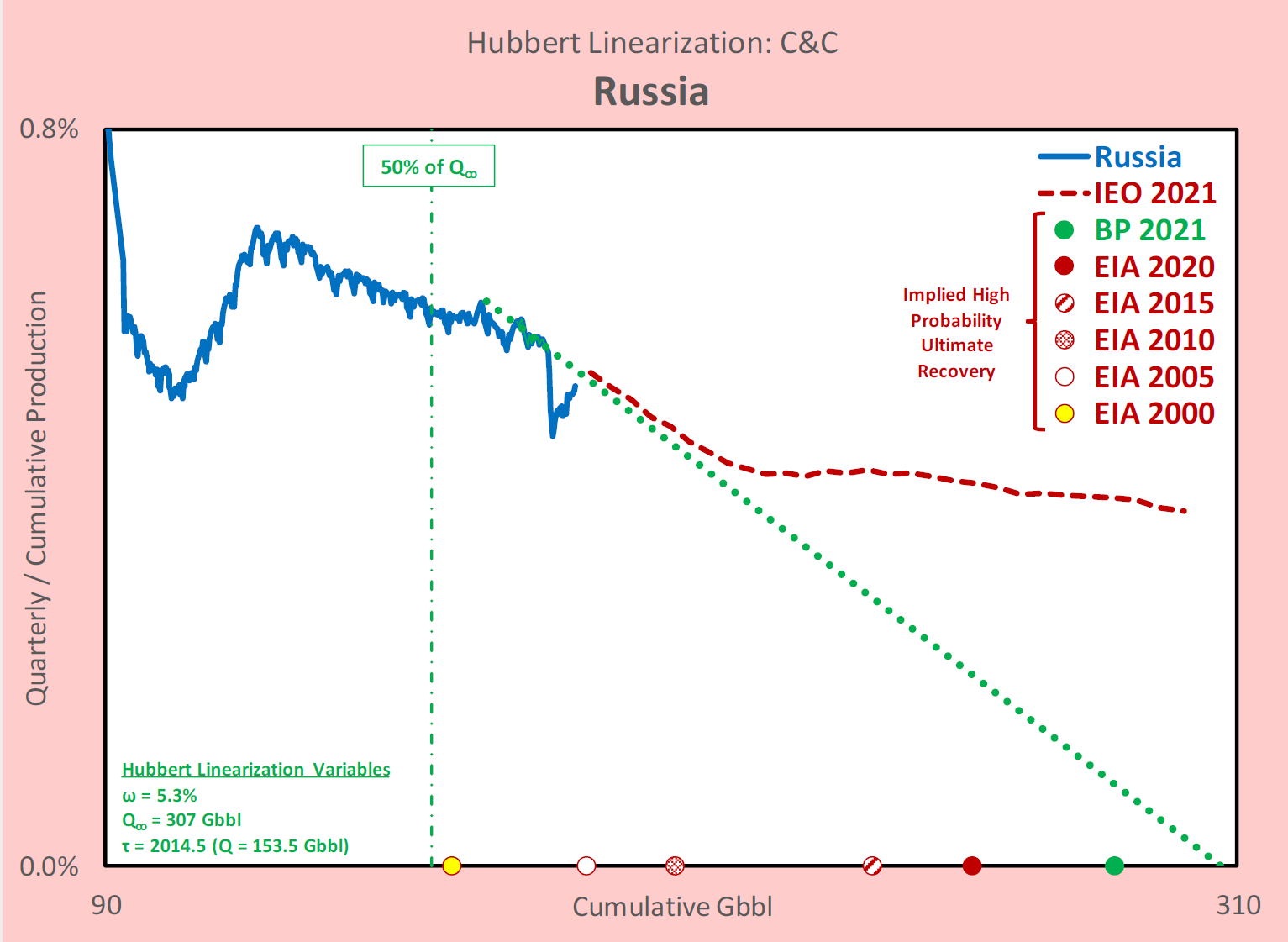

Hubbert linearization is evaluated by plotting the ratio of the sum of three months (i.e., quarterly) production by the then current cumulative production. This is plotted against cumulative production. The Hubbert projection ultimate recovery is where the linear extrapolation (green dotted line) intersects the x-axis. For comparison purposes, the sum of cumulative production and reserves for various years is also plotted, these being referred to as implied high probability estimates of ultimate recovery (EUR). These estimates may not include probable, possible or speculative resources and do not include yet-to-find. Also plotted is EIA’s forecast, transformed into Hubbert Linearization format. For non-industry readers, Gbbl is an abbreviation for billion barrels.

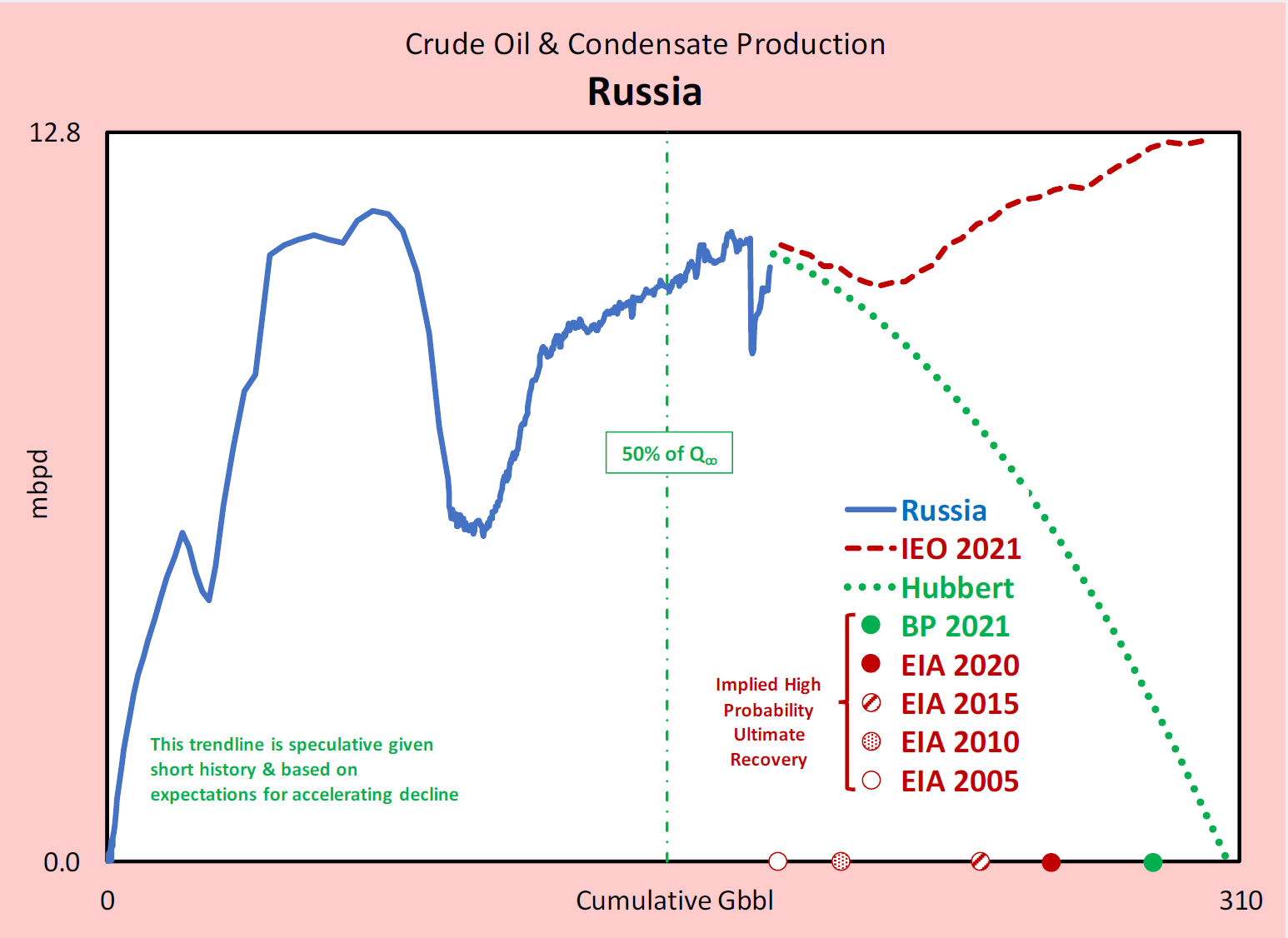

The Hubbert Projection can easily be transformed into a rate versus cumulative production format, which is presented below. Note that if EIA or BP’s reserve estimates are more accurate estimates of ultimate recovery, the Hubbert Projection would be steeper and the decline rate more severe. “mbpd” is an abbreviation for million barrels per day.

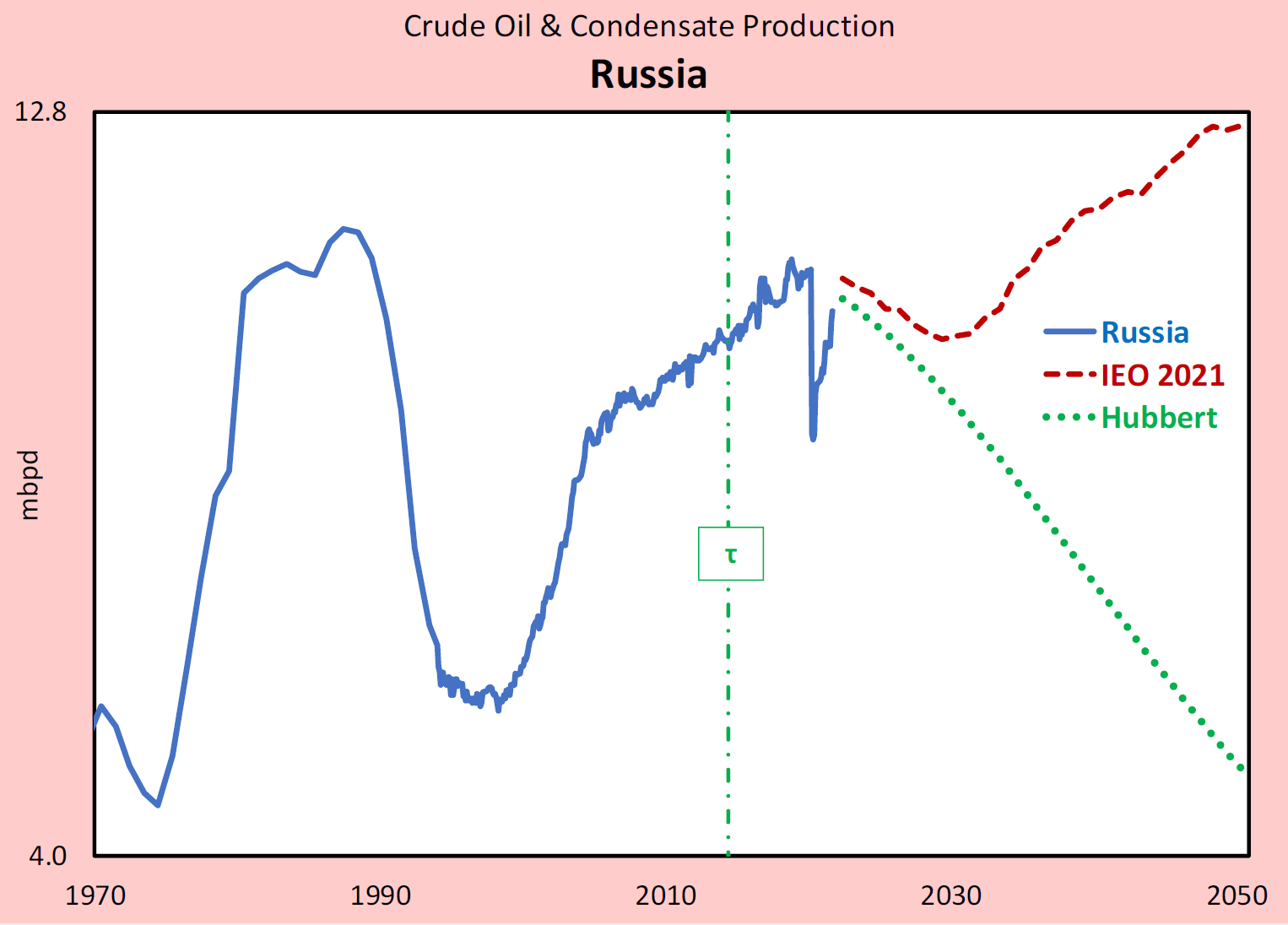

The last step is to transform the Hubbert projection into a time-series, which is done using an equation presented in Claerbout and Muir’s paper.

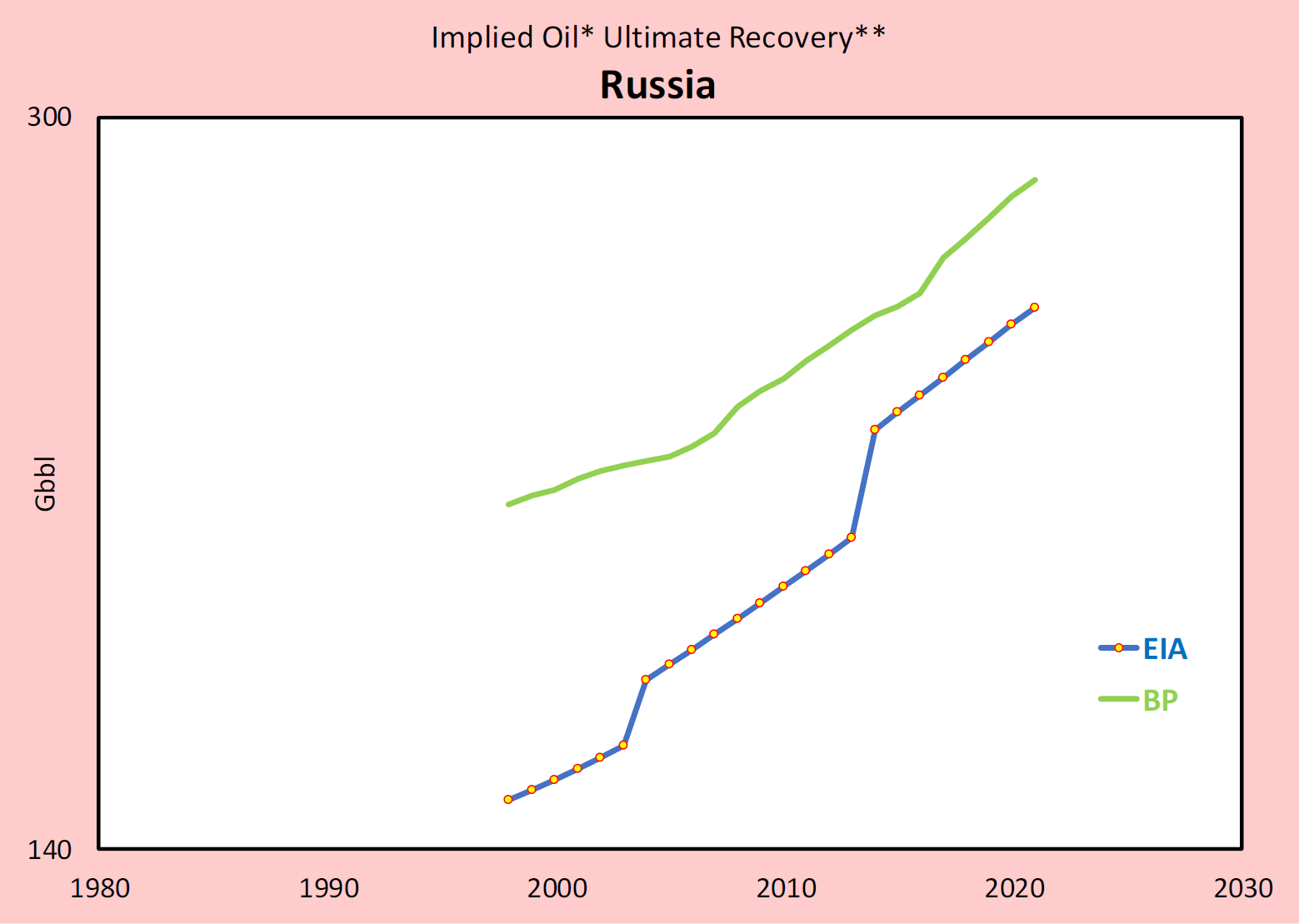

For those that are curious, the plot below is a history of the high probability ultimate recovery implied by EIA and BP’s reserve estimates.

Summary

Hubbert Math suggests that depletion of Russia’s initial economic oil resources is currently at least 59% and could be greater if EIA or BP’s implied ultimate recovery estimates are more accurate. EIA’s IEO 2021 forecast assumes that Russia commercializes West Siberian tight oil or Arctic oil by 2030. This is highly speculative and unlikely if Western sanctions persist.

One possible reason for Russia invasion of Ukraine is that cannot rely on income from domestic oil (and gas) production to finance its government (and in particular, its military). Ukraine is not a significant oil producer, but it is otherwise a resource-rich country. If Russia intends on defending its borders into the distant future, it must find new sources of revenue.

I agree with Greg B.'s analysis and prognostication. Russia would not invade Ukraine simply for political reasons. The Soviet Union existed long ago, was not sustainable and it is not likely that political leaders in Russia would believe they could resurrect it. So, there must be something in Ukraine that Russia wants to control. Another factor to dismiss is that Russia had any fear the Ukraine would try to somehow harm Russia. There are two resourcess to consider here, products and business capacity.

Russia and Ukraine have a free trade agreement. Thus, they already trade commodities and products freely. In fact, Ukraine purchases almost 6 billion dollars of petroleum products from Russia currently. Russia purchases enormous amounts of agricultural products from Ukraine. Seeemingly, for trade, Russia has no incentive to occupy Ukraine.

Ukraine has been steadily moving towards a business model more closely aligned with the European Union and other free, democratic nations. This puts Russia's international business model on a collision course with its neighbor and trading partner. The 'Westernization' of Ukraine's business practices' is an existential threat to Russia. To the extent that Russia is bordered on Europe and its open business practices and on China with its closed business practices, Russia is quite likely to be squeezed. This economic reality is quite likely to cause an enormous pressure on Russia to reform its business practices, or to become more economically challenged that it is now.

Although issues related to petroleum products must have a major impact on Vladimir Putin's thinking, I believe that Putin invaded Ukraine because he is against 'Westernization' and he wants control of Ukraine's business practices.

C.